This article was produced in partnership with ProPublica.

Since Donald Trump’s election, federal white-collar enforcement has taken a big hit. Fines and settlements against corporations have plummeted. Prosecutions of individuals are falling to record lows.

But just how these fines and settlements came to be slashed is less well understood. Two settlements with giant banks over financial crisis-era misdeeds provide a window into how the Trump administration has eased up on corporate wrongdoers.

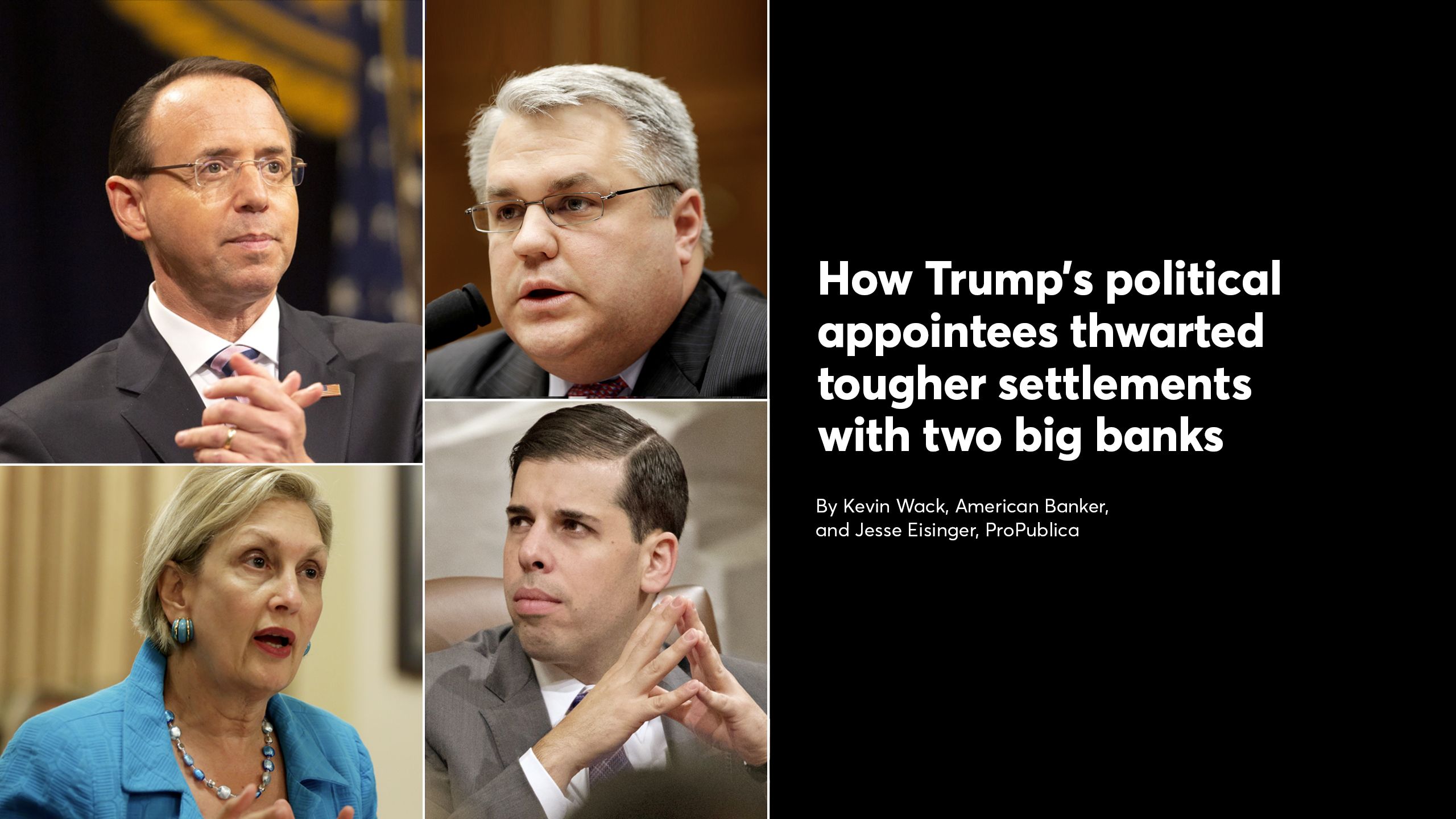

In settlements last year with the two big U.K.-based banks, Barclays and Royal Bank of Scotland, political appointees at the Trump administration Justice Department took the unusual step of overruling staff prosecutors to reduce the settlements sought, leaving billions of dollars in potential recoveries on the table, according to four people familiar with the settlements.

In the case of RBS, then-Deputy Attorney General Rod Rosenstein decided that the charges should not be pursued as a criminal case, as the prosecutorial team advocated, but rather as a less serious civil one.

Both cases were developed by the Obama administration DOJ and involved accusations that the banks misled buyers of residential mortgage-backed securities before the 2008 financial crisis. Prosecutors seemingly found numerous examples of bankers knowingly selling lemons to their customers. The mortgages they were putting into securities were “total fucking garbage,” one RBS executive said in a phone call that was recorded and cited in a DOJ filing. A Barclays banker said a group of loans “scares the shit out of me.” Mortgages that went into the two banks’ securities lost a total of $73 billion, according to calculations used by the government.

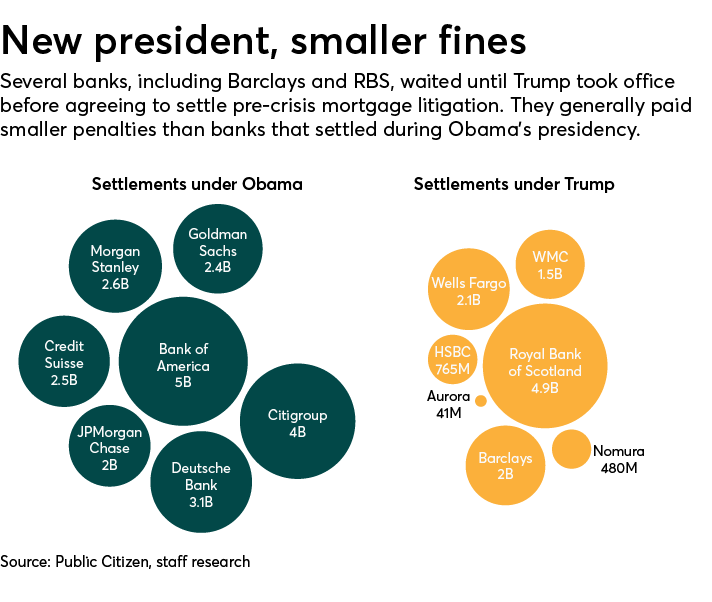

In March 2018, the DOJ settled with Barclays for $2 billion, a sum dictated by Trump appointees that was far below what the staff prosecutors in the Eastern District of New York in Brooklyn had sought. The settlement with RBS occurred in August 2018, for $4.9 billion. After Rosenstein downgraded the case from criminal to civil, other Trump appointees concluded that the settlement amount should be about half of what staff prosecutors in the District of Massachusetts had sought.

After a meeting with RBS lawyers, then-Deputy Attorney General Rod Rosenstein told the U.S. attorney in Boston not to pursue criminal charges.

DOJ spokeswoman Sarah Sutton said that the Barclays and RBS settlements held the banks accountable for serious misconduct, and that the penalties recovered from the banks were fair and proportionate compared with those previously obtained from other banks. She did not respond to detailed questions about how the two settlements were reached and why key decisions were dictated from Washington. “They were largely negotiated by career attorneys in the Department and U.S. Attorneys’ offices with the support and collaboration of Department leadership,” Sutton wrote in an email.

Aspects of how the DOJ came to settle the cases have been recounted. The New York Times reported on Rosenstein’s decision in the RBS case. But this is the first extensive account of how the banks secured the favorable outcomes.

The British banks employed an old playbook, one that proved effective with the Trump administration: Hire prominent former high-level DOJ officials who were now at major law firms. These attorneys won access to the top echelons of the Trump DOJ, where they found an audience receptive to their arguments that the staff prosecutors were unfairly singling out their clients for excess punishment.

The two cases stemmed from the Obama administration’s efforts to bring charges against banks for misdeeds that contributed to the financial crisis. Critics assailed the Obama DOJ for what they perceived as tardy and inadequate policing of financial crisis malfeasance. For example, the Obama DOJ did not prosecute any top bankers for actions related to the crisis. But it did belatedly bring civil charges, and it reached large settlements with numerous banks, including JPMorgan Chase, Citigroup and Bank of America. Moreover, the Obama-era DOJ consistently required the banks to acknowledge their bad acts, a practice that has ceased during the Trump administration.

As the Obama administration was winding up in the fall of 2016, the DOJ had not completed all that it aspired to. It rushed to reach settlements with foreign banks that had shown less urgency to resolve the allegations than some of their U.S. counterparts.

Less than a week before Trump’s inauguration, the DOJ announced that Deutsche Bank had agreed to pay a $3.1 billion civil penalty, and that Credit Suisse would pay $2.48 billion. But there were holdouts, including Barclays and RBS.

Barclays bets on Trump

Prosecutors in Brooklyn wanted Barclays to pay somewhere within a range in the high single digits of billions of dollars, according to two people familiar with the negotiations. Barclays balked, drawing a line at $2 billion, according to a Bloomberg News account.

Barclays hired an all-star team of defense lawyers. The roster included Karen Seymour, a partner at Sullivan & Cromwell who had previously served as chief of the criminal division in the U.S. attorney’s office in Manhattan and has since become general counsel at Goldman Sachs.

Also on Barclays’ legal team was Kannon Shanmugam, a former high-ranking official in the George W. Bush DOJ who was then a partner at Williams & Connolly.

With the two sides far apart in December 2016, the DOJ sued Barclays. Prosecutors also brought civil charges against two former executives at the bank who played key roles in its pre-crisis subprime mortgage operations.

Suing was an unusual step — cases against large corporations normally settle before a complaint is filed — and it was meant to send an implicit message to Barclays. Because the DOJ had been forced to go to court, the British bank could expect the price tag of an eventual settlement to be higher.

Barclays was making the opposite bet: that it would be able to negotiate a more favorable settlement once Trump appointees were in place at DOJ.

In a 192-page complaint, the DOJ alleged that Barclays engaged in fraud on a massive scale, deceiving investors about the characteristics of mortgages used to create securities that sold for tens of billions of dollars.

Barclays was accused of deceiving investors about the quality of mortgages that it used to create securities. More than half of the loans eventually defaulted, the government alleged.

A Barclays employee commented during a 2006 phone call that one particular pool of mortgages was "about as bad as it can be," but he did not abandon the loans or modify the bank's standard disclosures to investors, according to the government's complaint. In another example, when that same banker said that a particular pool of loans "scares the shit out of me," because he believed the company that originated the mortgages was likely to go bankrupt soon, Barclays bought the loans anyway. The bank deliberately did not conduct due diligence on the mortgages and then packaged them into bonds, the complaint asserted, all the while falsely telling a rating agency that due diligence had been done on 100% of the loans.

“More than half of the underlying loans defaulted,” the complaint stated, causing huge losses for investors.

Barclays’ legal team argued that the bank should not pay higher penalties in a settlement than other banks had paid relative to their market share. Barclays had been a relatively small player in the residential mortgage-backed securities, or RMBS, market, and its settlement should be sized accordingly, they reasoned.

This was an argument that the DOJ had long rejected. In a 2014 speech, then-Associate Attorney General Tony West argued that a firm’s market share should not outweigh evidence of the extent of its wrongdoing. “The facts and evidence of a particular case — they are what will ultimately matter the most,” he said.

In the Barclays matter, prosecutors in Brooklyn believed they had a strong case. The judge assigned to the case, U.S. District Judge Kiyo Matsumoto, seemed to agree. “This complaint is probably one of the more fulsome complaints I’ve ever seen,” Matsumoto said at an April 2017 hearing.

But the view that ultimately mattered was the one held by a new crop of officials at Main Justice, the DOJ’s headquarters in Washington. Besides Rosenstein, who was not involved in the Barclays case, key players in the RMBS settlements included Trump administration political appointees in the associate attorney general’s office, according to people familiar with the talks.

Steve Cox, the deputy associate attorney general, oversaw the cases, reporting to Jesse Panuccio, the principal deputy associate attorney general. In February 2018, Panuccio became acting associate attorney general, the No. 3 position at the DOJ, after Rachel Brand resigned from the post.

Note: Shows civil penalties that banks committed to pay in mortgage settlements with the DOJ; commitments to compensate consumers in Obama-era settlements, which may not reflect actual outlays by the banks, are excluded.

Note: Shows civil penalties that banks committed to pay in mortgage settlements with the DOJ; commitments to compensate consumers in Obama-era settlements, which may not reflect actual outlays by the banks, are excluded.

Neither had much experience with federal prosecutions. Panuccio was a former lawyer to Florida Gov. Rick Scott, as well as the chief labor and land use official in Florida, and Cox was a onetime associate at WilmerHale who had spent six years as a corporate counsel at an oil company, Apache Corporation, before joining the DOJ.

Following communications with the Barclays legal team, DOJ officials in Washington conveyed a message to the staff prosecutors in Brooklyn: settle the case within a narrow range around $2 billion, or we will take the negotiations out of your hands. The instruction came via a spreadsheet that listed the dollar range.

For DOJ officials in Washington to dictate specific terms of a settlement was unusual. U.S. attorney offices generally have wide latitude in choosing what they investigate and in making prosecutorial decisions. “Involvement of DOJ in cases handled in the U.S. attorney's offices is not common” but happens on big cases from time to time, said Harry Sandick, a former federal prosecutor who is now a partner at Patterson Belknap. During Obama-era negotiations, Main Justice had tried to show a united front with prosecutors who’d investigated the RMBS cases, according to former department officials.

Jesse Panuccio, a Trump political appointee at DOJ, sat in a key position as Barclays and RBS were negotiating settlements with the department in 2018.

At least one prosecutor acknowledged the internal rift between Brooklyn and Washington to the Barclays’ defense team, according to a source familiar with the matter. Once prosecutors in Brooklyn learned Main Justice’s position, this prosecutor communicated to the Barclays side that the bank had prevailed. Recalling how the deal went down, one government official said: “It seemed like a defeat.”

The staff prosecutors weren’t just disappointed about settling for a fraction of what they had sought back in 2016. They had brought civil charges against two former Barclays employees, Paul Menefee and John Carroll, and in exchange for dismissal, the two men agreed to pay a combined $2 million. But the agreement did not include language that precluded Barclays from footing the bill. That meant that Menefee and Carroll, who did not admit wrongdoing, might not have to pay a dime out of their own pockets.

Lawyers for Menefee and Carroll did not respond to requests for comment. In a statement, U.S. Attorney Richard Donoghue said, “The substantial penalty Barclays and its executives had to pay was an important step in recognizing the harm that was caused to the national economy and to investors in RMBS.”

At Main Justice, at least one official also regretted the Barclays deal, but from the opposite perspective. Cox told a prosecutor that he wished the Barclays settlement had been even smaller, but he explained that it wasn’t feasible to go lower because it had been reported that the bank offered to pay $2 billion, according to a person familiar with the conversation.

Cox did not respond to requests for comment.

Panuccio, who stepped down from the DOJ in the spring, declined to answer specific questions, citing the confidentiality of the department’s process. In an email response, he said, “The general narrative the questions seem to suggest is belied by the facts — including the fact that DOJ recovered historically significant sums in its 2018 and 2019 FIRREA settlements, and the fact that DOJ filed a major FIRREA suit against UBS in November 2018.” (FIRREA is the Financial Institutions Reform, Recovery and Enforcement Act of 1989, a law dating from the savings and loan scandals of the late ’80s.)

Barclays declined to comment.

Federal prosecutors in Boston wanted to bring criminal charges against the Royal Bank of Scotland. The bank’s lawyers argued that RBS should not be treated differently from other banks that faced only civil charges.

RBS escapes criminal heat

While Barclays had been in active negotiations with the DOJ during the Obama administration, the RBS defense team had not. RBS did not want to enter negotiations until the prosecutors dropped the criminal investigation.

Boston prosecutors declined to do so. Mortgages that went into RBS’ securities suffered about $54 billion in losses, ravaging their customers’ investments. The prosecutors believed they had compiled damning evidence that RBS officials knew what they were doing was wrong. In one example, RBS’ chief credit officer in the United States called the mortgages that were going into the securities “total fucking garbage” with “fraud [that] was so rampant ... [and] all random,” according to calls the prosecutors later quoted in the statement of facts against the bank. He stated that “the loans are all disguised to, you know, look okay kind of ... in a data file.”

In 2016, the RBS defense team, which included former Deputy Attorney General Jamie Gorelick, of WilmerHale, appealed to Stuart Delery, then the third-highest official at the DOJ. Delery knew Gorelick from their time at the DOJ. Despite that relationship, according to a person knowledgeable about the matter, Delery said he would not interfere with an ongoing investigation at a U.S. attorney’s office. (Delery did not respond to requests for comment. Gorelick directed questions to RBS.)

Then came November. A few months later, the Trump appointees arrived.

For a while, nothing changed. The Boston prosecutors continued their investigation, more convinced than ever that the RBS conduct merited a criminal charge. They wrote what’s known as a “prosecution memo,” which they had begun during the Obama administration, describing the underlying criminal acts under FIRREA.

Such a move would have been groundbreaking. The Obama DOJ had used FIRREA, but for civil charges. And the Boston prosecutors did not want to stop there. They argued for first charging the bank criminally, and then moving on to seek criminal charges against individual bankers. Those would have been the first of their kind.

They never got that far.

Jamie Gorelick of WilmerHale, a former deputy attorney general in the Clinton administration, represented RBS. She had connections to high-level DOJ officials during both the Obama and Trump administrations.

In time, Trump political appointees such as Panuccio and Cox began to figure out their way around the department. The RBS defense team, including Gorelick, requested meetings with top officials. Gorelick again had a connection with a key DOJ official. She had worked with Cox, earlier in his career when he was an associate at WilmerHale, defending BP in investigations of the Deepwater Horizon spill.

The defense group now also included Mark Filip of Kirkland & Ellis, representing the British government's interest in RBS. Filip, who did not respond to requests for comment, has a special stature. During his tenure as deputy attorney general, he had codified the conditions prosecutors had to assess in bringing cases against corporations, which are today known as the “Filip Factors.” Prosecutors are supposed to weigh a variety of issues, such as how serious offenses are and whether the company has cooperated with investigators. As a private sector big hitter, companies hire him, in the view of prosecutors, to explain why his factors are not met in a given case.

The RBS team was able to meet with the No. 2 at the DOJ, Rosenstein. It’s unusual, though not unprecedented, for a defense team to get access to such a high-level official. The RBS team persuaded Rosenstein.

In the spring of 2018, Rosenstein informed Andrew Lelling, the U.S. attorney for the District of Massachusetts, that his office couldn’t pursue criminal charges against RBS. Rosenstein said he didn’t want the DOJ treating RBS differently from other banks, which faced only civil investigations. (The Massachusetts U.S. attorney’s office declined to comment on the details of the RBS settlement. Rosenstein, who left the DOJ in May, did not respond to inquiries.)

RBS spokeswoman Linda Harper confirmed that the Boston U.S. attorney’s office had recommended criminal prosecution and that the bank had met first with Delery and then with Rosenstein.

Mark Filip, a former deputy attorney general, was part of the RBS defense group, representing the British government’s interest in the bank.

“The argument we made was for fairness and parity,” she said. The bank’s defense team, she added, argued that “Main Justice should ensure that like cases are treated alike.”

The Boston team was disappointed and angry. It argued that prosecutors charge people when they have the necessary evidence, even if they cannot charge all people who committed the same crime. And it maintained that the decision went against department policy. In May 2017, then-Attorney General Jeff Sessions issued a memo directing prosecutors to charge defendants with the most serious provable crimes carrying the highest penalties.

“It calls into question whether the memo meant what it says when it came to white-collar prosecutions,” a person familiar with the decision said.

Once the case was downgraded, the Boston team turned to deciding on the monetary settlement. Internally, prosecutors had discussed seeking a settlement in the $9 billion to $10 billion range, reflecting their belief that the RBS conduct was especially egregious.

At one point in the spring after the Rosenstein meetings, Main Justice sent Boston a similar spreadsheet that it sent to other U.S. attorney offices concerning their open cases, including those against Barclays, Japanese bank Nomura and Swiss bank UBS. For RBS, the range was between around $4.5 billion to about $6.6 billion.

The Boston prosecutors tried to get the settlement as close to the top of the range as they could. But they were thwarted even in that attempt. Cox told the Boston team that the DOJ would “call the bluff” of RBS and tell the bank it would take $4.9 billion.

Prosecutors thought the DOJ had caved. They complained to Cox that Main Justice had authorized the office to seek as much as $6.6 billion. Cox’s reply: RBS won’t go that high.

Photos: Bloomberg News and Getty Images

Like what you see? Make sure you're getting it all